Colin Nagy | March 20, 2020

Why is this interesting? - The WeChat edition

On app ecosystems, convergence, and quick iterations

Colin here. WeChat is an endlessly fascinating platform. If we set aside the very real privacy concerns for a moment, it really is a one-of-a-kind service—and something US tech giants are clearly looking to for inspiration. The app is fast, lightweight, and often unbeknownst to those who use the watered-down US-version, it allows Chinese speakers and Chinese nationals to do basically everything they need to do in life, all in one place. There’s an array of mobile services, from payments to filing court paperwork to sending money, to ordering food or a car to booking a vacation. One of the superpowers (and accelerants) is the launch of mini-programs in 2017.

The Times explains:

In the two years since then, businesses have created more than a million of them, equal to half the number of iOS apps available in Apple’s App Store. They come from global conglomerates like McDonald’s and Tesla and from local businesses like restaurants, hair salons and gyms. All of them are drawn in by the gravitational pull of WeChat’s enormous number of users and its standardized software infrastructure. It resembles the European Union in the way it has evolved into a market ecosystem: Miniprogram developers benefit from a common currency (WeChat’s mobile payment system), an identification system (WeChat’s login and password) and greatly lowered barriers to trade and movement (easy integration with any number of other services on WeChat). Because miniprograms run inside WeChat, businesses’ customers don’t have to sign up, log in or add their credit card numbers.

The rest of the world is watching. And when you see the work that Mark Zuckerberg has done to integrate Facebook, Whatsapp, and Instagram, one can squint and see a future of Western world “super apps” and regardless, as the Times states, "WeChat internet is almost certainly a glimpse of what comes next.”

Why is this interesting?

The strategy is simple. Build atop the utility where everyone is spending their time. Is it happening on other messaging apps outside China?

It turns out that some entrepreneurs are building minimum viable products on top of Whatsapp, the messaging platform that is widely used in other parts of the world. A partner at Antler, a VC in Southeast Asia explains:

We now see a similar trend in Southeast Asia. Here, WhatsApp is the dominant social platform and, while it has not built the same infrastructure for building apps, startups have found a way around that and now run many services on top of WhatsApp, validating with customers quickly and cheaply. These companies are not only mobile-first, but they are also WhatsApp-first… Sama, which on-boards construction workers seeking jobs abroad on Facebook Messenger and WhatsApp, anticipated at the outset that there would be possibilities to enable financial inclusion in its recruitment model. If you are logging someone’s identity and can prove they have worked, you eliminate a majority of challenges working with financial and utility companies. The immediate development they saw was cooperation with telcos and online remittance companies. Many of Sama’s users rely on weekly prepaid SIM cards due to a lack of documents and payment methods (most telcos want credit cards and utility bills).

Sama is an interesting company seeking to solve problems and abuse in the migrant labor community. They realized that an MVP of their product didn’t need to reinvent the wheel when reaching potential customers, opting to reach them where they were spending their time: on their phones, via the preferred channel. Why build the tech when you can draft off of an existing habit and build services around it?

Now, this doesn’t mean that there’s an existing ecosystem or even the ability to build apps within WhatsApp, but rather it is interesting that small scrappy startups with a good idea can tap into the energy and utility to start building their products. (CJN)

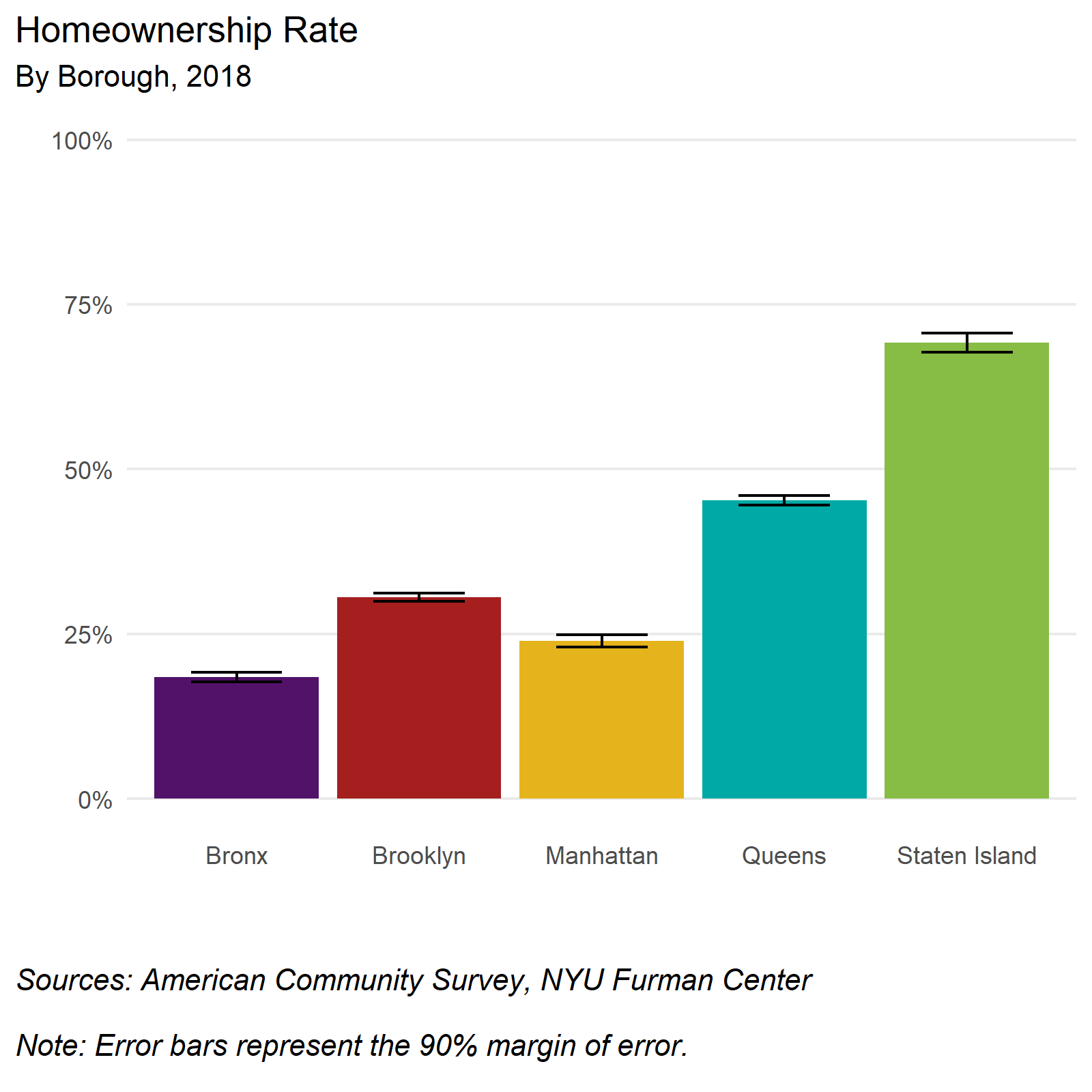

Chart of the Day:

Some data from NYU’s Furman Center: “In 2018, the New York City homeownership rate was 33 percent, but it varied by borough. The homeownership rate in Staten Island was 69 percent, far closer to the national rate (64%) than any other borough. The Bronx had the lowest homeownership rate at 18 percent, approximately 45 percentage points lower than the national rate. Queens had a homeownership rate of 45 percent, Brooklyn 30 percent, and Manhattan 24 percent.” (NRB)

Quick links:

A survival story for the ages (CJN)

What we lose when a favorite restaurant disappears forever (CJN)

Heterogeneous Compute: The Paradigm Shift No One is Talking About (NRB)

Thanks for reading,

Noah (NRB) & Colin (CJN)

Why is this interesting? is a daily email from Noah Brier & Colin Nagy (and friends!) about interesting things. If you’ve enjoyed this edition, please consider forwarding it to a friend. If you’re reading it for the first time, consider subscribing (it’s free!).